Market Outlook

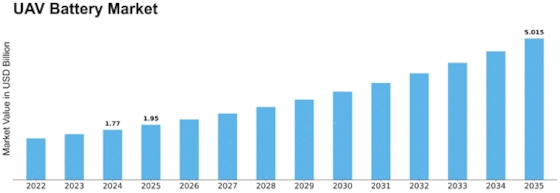

The global market for batteries used in UAV Battery Market is poised for strong growth over the coming decade. According to recent data, the UAV battery market was valued at approximately USD 1.61 billion in 2023, and is projected to climb to around USD 5.0 billion by 2035, representing a compound annual growth rate (CAGR) of about 9.9%. This expansion is underpinned by rapidly increasing adoption of UAVs in industries such as agriculture, logistics, defence, environmental monitoring and commercial inspection.

Industry Overview

UAVs (also referred to as drones) place unique demands on energy storage systems: light weight, high energy density, long flight times, and often rapid recharging. As UAV deployments move beyond hobbyist use into industrial, agricultural, governmental and military settings, the requirements for batteries shift accordingly. Advances in battery chemistry (lithium-ion, lithium-polymer, fuel cells, etc), improvements in battery management systems (BMS), and evolving regulatory frameworks all converge to transform the underlying battery market. According to analysis, technological innovation and sustainability pressure (lighter, greener batteries) are also major drivers.

Key Players

Within the UAV battery market, several companies stand out. For example:

- VARTA AG (Germany): Known for its lithium-ion batteries tailored for UAV applications, offering compact and durable solutions.

- Ballard Power Systems (Canada): Has announced next-generation fuel-cell modules for UAVs, addressing long-endurance missions.

- Sion Power Corporation (USA): Introduced a lithium-metal “Licerion” battery targetting UAVs, aiming to boost energy density.

- Others: LG Energy Solution, Samsung SDI, Saft Groupe, A123 Systems, among a broader competitive field.

Segmentation Growth

Growth in the UAV battery market is being driven across several segmentation axes: - By Application: The market covers military, commercial, agricultural and environmental monitoring use-cases. For instance, the military segment was around USD 0.55 billion in 2024 and is expected to rise to around USD 1.55 billion by 2035.

- By Battery Type: Lithium-ion remains dominant due to its favourable energy density/weight trade-off, with lithium-polymer also gaining traction for specialized UAVs. Lead-acid and nickel-cadmium remain marginal for cost-sensitive or legacy systems.

- By Voltage Range: UAV batteries are segmented into ranges such as below 12 V, 12-24 V, 24-48 V, and above 48 V, reflecting varied mission profiles from lightweight hobby drones to heavy-lift industrial systems.

- By End Use: End use spans private (hobby/recreational), governmental (surveillance, public safety) and industrial (logistics, agriculture, infrastructure inspection). Growth in industrial and governmental use is particularly strong as businesses and agencies adopt UAVs for productivity gains.

Closing Thoughts

As UAV adoption continues to accelerate, the battery market underpinning these systems will increasingly become a strategic battleground. Manufacturers and component suppliers who innovate in energy density, flight duration, cost-effectiveness and safety will capture disproportionate value. For companies looking to partner, invest or compete in this space, the coming decade offers rich opportunity.